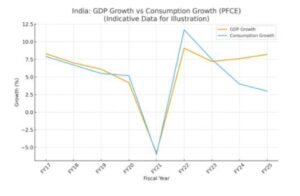

India GDP growth: India’s latest GDP figures have reshaped the macroeconomic debate. Growth came in at 8.2% for FY25 and 7.5% for Q2, defying expectations and reaffirming India’s status as the world’s fastest-growing major economy. The announcement triggered enthusiasm in markets and policy circles because it arrived amid global uncertainty, tightening credit conditions and patchy recoveries in advanced economies. The argument centres on whether this pace reflects a broad-based economic boom or a cyclical surge driven by a narrow set of performers.

The evidence shows that India’s national accounts have become more volatile in recent years, as noted by the IMF, which retained India’s “C” rating for data transparency in 2024. The constitutional question is whether headline GDP growth alone can guide policy when private investment, consumption and job creation display uneven trends. This op-ed evaluates the drivers of the 8.2% surge and examines its durability.

READ | AI is transforming news, search, fact-checks and feeds

GDP growth: Structural upswing or one-off spike?

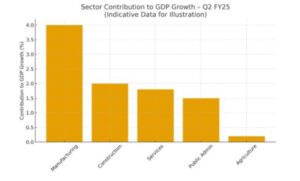

Manufacturing emerged as the standout performer, expanding at over 12%, supported by strong corporate profits, PLI-linked sectors and improved supply-chain resilience. Some high-frequency indicators reinforce this momentum: core sector growth touched a four-month high, steel output expanded sharply, and cement production remained firm. RBI’s corporate performance dataset also shows rising margins, especially in automobiles, electronics and capital goods.

However, the policy concern is whether manufacturing strength is broad or concentrated. Capital goods imports have risen, but private capex remains lopsided and driven by a handful of large firms. Bank credit to industry grew by 8–9%, but micro and small enterprises continue to face tight financing conditions. Capacity utilisation in manufacturing climbed to 74%, close to the long-term average but not signalling overheating or a major investment surge.

Public capex has played an outsized role: central government capital expenditure rose by over 16%, sustaining construction and materials. Yet this raises institutional questions on crowding-in. Sustainable manufacturing growth depends on deeper reforms—dispute resolution, logistics efficiency, stable power availability and predictable taxation—areas that require state-level coordination.

Weak demand behind strong GDP?

Private consumption grew only 3%, well below pre-pandemic averages. Urban discretionary demand held up, reflected in airline traffic, premium vehicle sales and hotel occupancy levels. But rural demand stayed weak. Two years of erratic monsoons, high food inflation and stagnant real wages meant that consumption’s contribution to GDP was muted. FMCG companies continued to report volume pressures, and rural mobility indicators remained below trend.

Labour market data presents a mixed picture. Payroll enrolments improved, but the PLFS reports a persistent rise in self-employment and unpaid family work. The policy concern is whether job creation is keeping pace with the younger labour force. Without broad-based employment gains, consumption cannot power sustained 8% growth.

A related issue is inequality in the consumption rebound. Listed company profits surged to historic highs, but household savings fell to a decadal low of 5.3% of GDP, according to RBI data. The substitution of financial savings with debt-funded consumption poses macro-stability risks if interest rates stay elevated.

Public spending and data quality

Government expenditure remained a central pillar of the GDP print. Public administration, defence and other services grew above 7%, while infrastructure spending by the Centre and states supported construction. Government-led growth stabilises the economy in times of global uncertainty, but it also complicates assessment of private-sector momentum.

A growing concern in global and Indian commentary relates to the quality of national accounts. Divergences between GDP and GVA, overstated deflators, and inconsistencies in labour income estimates have been flagged by analysts. The IMF’s recent assessments emphasise the need for improved expenditure-side data and more reliable household surveys.

The constitutional question is whether growth measurement should rest on indicators that mask stress in consumption and employment. While India remains a standout performer globally, the credibility of data improves policy design, investor confidence and state-level fiscal planning.

Trade and external sector

Exports of goods contracted for part of the year, but services exports continued to anchor the external account. Software and business services grew strongly, and tourism receipts improved with global travel normalisation.

The rupee remained stable despite global volatility. RBI reserves crossed $660 billion, providing a buffer against oil price swings. However, structural risks persist. Electronics imports continue to rise faster than exports. Remittances may soften as labour markets in West Asia and North America slow.

The argument centres on whether India can build an export engine strong enough to complement domestic growth. Trade agreements, logistics reforms and sectoral competitiveness matter more now, given the protectionist turn in advanced economies. Without a stronger external sector, the domestic cycle may face limits.

India’s 8.2% GDP surge is impressive and reflects genuine strengths in manufacturing, public investment and services exports. The economy has shown resilience despite global headwinds, elevated interest rates and geopolitical uncertainty. Yet the evidence shows an uneven recovery across households, sectors and states. Weak consumption, stagnant rural wages and limited private capex prevent the current cycle from becoming a structural boom.

The policy path must focus on improving data quality, strengthening state-level capacities, easing credit constraints for MSMEs and supporting labour-intensive sectors. A durable 8% growth path requires stronger jobs, deeper reforms and more transparent measurement. India has the momentum—but the foundation must be broadened.