When the Sovereign Gold Bonds scheme was launched in 2015, it sought to correct a familiar imbalance in India’s macroeconomy. Households preferred physical gold over financial assets, pushing up imports, widening the current account deficit, and locking savings into an unproductive store of value. SGBs were meant to change this behaviour. Nearly a decade later, the scheme has delivered spectacular gains to investors — but at a rising fiscal cost that the government did not fully anticipate.

The redemption of the sovereign gold bond 2017–18 Series XIII at ₹13,563 per unit implies an absolute return of about 382% over eight years, excluding the additional 2.5% annual interest. For investors, this is a textbook example of patience being rewarded. For the government, it marks a moment of reckoning. A policy instrument designed to moderate gold imports has turned into a sizeable contingent liability amid a prolonged global bull run in the metal.

READ | What will drive gold prices in 2026 and beyond

The sovereign gold bond scheme

The logic behind SGBs was straightforward. By offering gold-linked returns without storage or purity risks, the government hoped to divert demand away from physical gold. In return, it could borrow at a cost lower than conventional market debt, while reducing pressure on the balance of payments. For several years, this arrangement appeared to work. Subscriptions were steady, gold imports moderated intermittently, and the interest burden remained manageable.

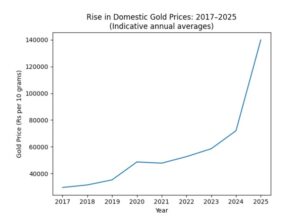

That balance has since shifted. From 2017 onwards, global gold prices rose sharply as central banks accumulated reserves, geopolitical tensions intensified, post-pandemic inflation surged, and confidence in fiat currencies weakened. Bonds issued at roughly ₹2,800 per gram are now being redeemed at more than ₹13,500. What was once a clever substitution mechanism has become an expensive obligation.

The payout burden has ballooned

The redemption value of a sovereign gold bond is linked to the simple average of the closing price of 999-purity gold for the three business days preceding maturity, as published by the India Bullion and Jewellers Association. This ensures full exposure to gold’s upside. Unlike market-linked instruments where investors bear price risk, sovereign gold bonds are sovereign liabilities. The Reserve Bank of India administers the scheme, but the fiscal burden ultimately rests with the Union government.

Over the years, multiple sovereign gold bond tranches—equivalent to several tens of tonnes of gold—have been issued. Each tranche carries two obligations: redemption at prevailing gold prices and a fixed 2.5% annual interest payment. With gold prices having more than quadrupled over the past decade, these liabilities have expanded sharply. While precise numbers vary, economists estimate that the mark-to-market value of outstanding SGB obligations now runs into several lakh crore rupees, creating pressure on future budgets.

READ | Gold prices signal India’s shift to digital wealth

A fiscal complication at the wrong time

The timing of these redemptions could scarcely be worse. The government is attempting fiscal consolidation without sacrificing capital expenditure or core welfare spending. Interest payments already absorb a large share of revenues, tax buoyancy remains uneven, and off-budget borrowings are under closer scrutiny. Against this backdrop, large SGB redemptions represent an additional fiscal shock. Resources that could have funded infrastructure, health, or education are instead being diverted to honour gold-linked commitments made years earlier.

There is also a behavioural irony at work. Far from weakening India’s affinity for gold, the strong performance of sovereign gold bonds has reinforced it. While equity markets have delivered volatile and uneven returns in recent years, SGB holders have been handsomely rewarded—by the state itself. The scheme’s success has sharpened public awareness of gold as a superior hedge, rather than nudging households decisively towards productive financial assets.

Accounting opacity, weak import impact

One reason the fiscal risks of sovereign gold bonds remained underestimated for so long lies in how they are treated in government accounts. Sovereign gold bonds are recorded as part of public debt at their issue value, while the much larger exposure arising from future gold price movements remains outside routine fiscal metrics. Budget documents do not present a consolidated picture of the mark-to-market risk embedded in outstanding SGBs. This creates a transparency gap. Unlike explicit borrowings, these liabilities surface only at redemption, complicating fiscal planning and weakening legislative oversight.

Equally important is the question of outcomes. There is limited evidence that sovereign gold bonds materially altered India’s dependence on gold imports. Annual gold imports have typically ranged between $35 billion and $45 billion in normal years, rising sharply during periods of price correction. Against this, cumulative SGB issuance measured in gold-equivalent terms has remained modest. The scheme may have shifted some investor preference at the margin, but it was never large enough to offset structural demand driven by jewellery consumption, rural savings behaviour, and cultural norms. In effect, the fiscal risk expanded faster than the macroeconomic benefit.

International comparison reveals the peculiarity of India’s approach. Major economies hold gold as part of central bank reserves, but few offer households fully gold-indexed sovereign instruments with open-ended payouts. Commodity-linked sovereign debt is generally avoided because it introduces volatility into public finances. By transferring gold price risk from households to the exchequer, India chose a path that is globally uncommon. That choice now calls for reassessment — not because the scheme failed investors, but because it exposed the state to risks that are difficult to manage in an uncertain global cycle.

READ | Gold price cools off, but the rally still has legs

Was the scheme flawed by design?

Sovereign gold bonds suffer from an inherent asymmetry. By fully indexing redemption to market prices while paying a fixed coupon, the government assumed all downside risk. In hindsight, design features such as partial indexation, a cap on capital gains, or a floating interest rate linked to gold prices could have limited fiscal exposure. Supporters counter that such constraints would have undermined investor appeal and defeated the objective of reducing physical gold demand.

The government’s response so far has been cautious. Fresh issuances have slowed, and greater reliance is being placed on gold monetisation schemes and import-duty adjustments. These tools, however, have had limited impact. Gold remains deeply embedded in Indian savings behaviour, shaped by cultural preferences and periodic distrust in financial markets during uncertain times.

For investors, the lesson is clear. SGBs delivered extraordinary returns in a specific global cycle marked by inflation, conflict, and currency anxiety. That outcome is not guaranteed to repeat. Gold prices can stagnate or fall, and future tranches may be structured less generously.

For policymakers, the lesson is more sobering. Financial innovation that is not stress-tested across extreme scenarios can create hidden fiscal traps. As gold-linked liabilities mature, the government will be forced to recalibrate its approach. The challenge will be to balance household preferences, macroeconomic stability, and fiscal prudence — without turning a well-intentioned policy into a recurring budgetary burden.