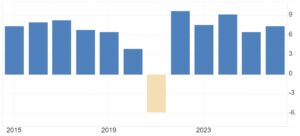

The International Monetary Fund has raised India’s FY27 GDP growth forecast to 6.4% in its latest World Economic Outlook. The revision brings the Fund closer to domestic projections that have turned more cautious as nominal expansion weakens. The upgrade also marks a slowdown from the 7.3% growth projected for 2025–26. For FY26, the headline looks stronger. A better-than-expected third quarter and firm momentum in January–March have lifted estimates. The National Statistics Office’s First Advance Estimates peg growth at 7.4%, up from 6.5% in 2024–25.

Policy discussions tend to stop there. The real GDP growth number is cited, the inference drawn, and the conversation moves on. What receives less attention is the widening gap between real and nominal growth now visible across official and multilateral projections.

The IMF’s upward revision for FY26, alongside the NSO’s advance estimates, points to an economy that has absorbed global turbulence better than many peers, supported by public capital expenditure, consumption, and a tentative recovery in private investment.

READ I Digital gender gap a drag on India’s growth story

Nominal GDP growth and fiscal math

The discomfort lies elsewhere. Nominal GDP growth, which matters for fiscal arithmetic, debt ratios, corporate revenues, and tax collections, looks far less robust. Advance Estimates suggest nominal growth of about 8% in FY26, the slowest since the pandemic years of 2020–21. This reflects an exceptionally low GDP deflator of around 0.5%—a five-decade low—signalling sharply cooled price pressures.

India annual GDP growth rates (%)

India’s real growth is therefore being flattered by low inflation rather than buoyant nominal incomes. For a developing economy, this divergence is unusual. Governments budget and borrow in nominal terms. Wages, profits, and tax bases are nominal. When nominal growth trails real growth by such a margin, headline strength does not translate into fiscal comfort or income buoyancy.

The IMF has noted that inflation is expected to return close to target after a marked decline in 2025, driven largely by subdued food prices. This has lifted real growth by compressing the deflator, but it has also narrowed nominal expansion. Lower inflation eases pressure on households and supports consumption; weak nominal growth strains revenue assumptions embedded in budgets.

READ I GDP deflator warning: How did the nominal growth weaken

Monetary policy, credit, and real interest rates

Low nominal growth also alters the monetary and financial transmission in ways that are easy to miss. When inflation falls faster than expected, real interest rates rise even without policy tightening. This implicitly tightens financial conditions, affecting credit demand, corporate borrowing, and the pace of private investment. For firms facing muted pricing power, higher real borrowing costs squeeze margins and discourage expansion. Households, too, face slower nominal income growth, which limits leverage and consumption despite favourable real growth metrics. In this setting, strong real GDP numbers can coexist with cautious lending behaviour and uneven credit transmission.

IMF chief economist Pierre-Olivier Gourinchas has warned that while global growth has held up despite trade disruptions, their effects will surface over time. India will not be insulated. Steep tariff actions by the United States add to external risk, especially for export-oriented sectors that also anchor employment and income generation. Pressure there will feed directly into nominal growth.

READ I Budget 2026: Fiscal policy debate ignores deepest structural flaws

Trade uncertainty and investment decisions

Trade uncertainty is already weighing on investment decisions. An environment of unpredictable tariffs and fragmented trade rules is hostile to long-term planning. Sustained friction would drag on both real output and nominal expansion over the medium term.

Private forecasters have been more circumspect than official agencies. Brokerages and research firms point to moderating corporate revenue growth and softening tax buoyancy despite healthy real GDP numbers. Low inflation is muting the top-line growth that firms and governments depend on.

State finances and demand constraints

India’s growth strategy over the past decade has leaned heavily on supply-side reforms, infrastructure spending, and productivity gains. These lift real output. Without sustained demand and pricing power, they do less for nominal expansion. State finances, more sensitive to nominal GDP assumptions and less able to absorb revenue shocks, are particularly exposed.

Real growth projections are not misplaced. But read in isolation, they are incomplete. High real GDP growth alongside weak nominal expansion complicates fiscal consolidation, narrows counter-cyclical space, and weakens the transmission of growth into incomes and jobs. As global risks accumulate, the reassurance of a single headline number can mislead.

Policy priorities are clear enough. Investment momentum and reform must continue to sustain real growth. But translating that into durable nominal expansion will require broad-based income gains, resilient demand, and some pricing power. Without that, the GDP growth numbers will look better on paper than they feel on the ground.