Study suggests India GDP mis-estimation: India’s GDP debate has often been reduced to a sterile choice between faith and disbelief. The new Peterson Institute for International Economics working paper, India’s 20 Years of GDP Misestimation: New Evidence, is useful because it avoids that trap. Its central claim is not that India’s statisticians fabricated growth. It is that the 2015 GDP methodology may have systematically misread the economy: understating the boom years before 2011 and overstating growth for much of the period after 2012. The charge cannot be dismissed as ideological. But neither should it be accepted as settled fact merely because it fits a popular intuition that the economy on the ground has felt weaker than the headline numbers suggested.

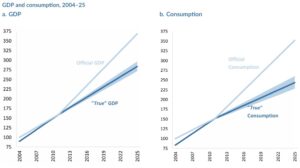

The paper, authored by Abhishek Anand, Josh Felman and Arvind Subramanian, makes two claims. First, the annual GDP growth between 2005 and 2011 may have been underestimated by roughly 1 to 1.5 percentage points. Second, the growth between 2012 and 2023 may have been overestimated by roughly 1.5 to 2 percentage points. The broad conclusion is that India did not experience two decades of stable, near-continuous high growth. While the economy experienced a genuine boom in the mid-2000s, it was followed by a prolonged deceleration after the global financial crisis and then a further hit from domestic policies such as demonetisation and the rollout of GST, and then from the pandemic.

READ I China’s 15th Five-Year Plan bets on tech-led global power

India GDP mis-estimation and the informal sector

The strongest part of the paper is not the exact size of the corrections. It is the diagnosis of where the old series went wrong. The authors argue that the 2015 framework relied too heavily on formal-sector data to estimate output in the vast informal economy. That may have been manageable in quieter times. It became much less defensible after 2016, when informal enterprises were hit harder than formal firms by demonetisation, GST compliance burdens, and then Covid. If the organised sector is used as a proxy when the unorganised sector is being damaged more severely, aggregate growth will look stronger than it really is. That proposition is not radical. It is economically intuitive. It is also consistent with what India’s labour market, small-enterprise distress and weak private investment had long been hinting at.

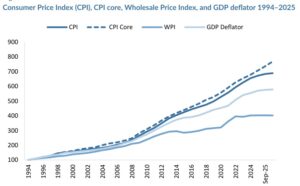

The second pillar of the paper concerns deflators, the price indices used to convert nominal output into real growth. Here too the criticism has force. If deflators are driven by wholesale or commodity prices, especially oil, while the relevant output prices behave differently, real growth can be flattered. India’s low GDP deflator in several recent years had already become a subject of unease because nominal growth looked modest while real growth remained surprisingly buoyant. The paper sharpens that unease into an empirical argument. It says that in parts of the post-2011 period, the inflation adjustment was simply too low, thereby overstating real expansion.

READ I Indian economy needs a hard oil shield

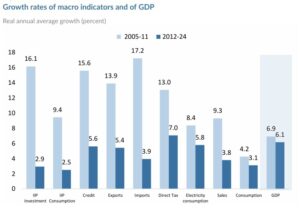

This is where the paper becomes harder to ignore. It does not rest only on statistical method. It points to a visible disconnect between GDP and a range of macro indicators. According to the authors, the mid-2000s boom was reflected across exports, credit, industrial production, tax revenues and investment. After 2011, most of these indicators slowed sharply even as official GDP continued to suggest a surprisingly stable growth trajectory. The paper reports, for example, that real credit growth fell from 15.6% to 5.6% between the two periods they compare; real exports from 13.9% to 5.4%; and IIP growth from 16.1% to 2.9%. When a national accounts series increasingly moves apart from credit, trade, tax and investment data, scepticism is not only legitimate. It is necessary.

Even so, a good economist should pause before converting a persuasive diagnosis into a precise alternate history. The paper’s magnitudes are reconstructed, not observed. They depend on proxy variables, backcasting exercises, and judgment calls about how the informal sector would have behaved relative to the formal sector. That is unavoidable in this kind of exercise. But it also means the revised numbers should be treated as informed estimates, not as a new official truth. The paper is probably more convincing on direction than on exact scale. It is easier to accept that post-2011 growth was overstated than to certify with confidence the precise degree of overstatement year after year.

READ I Market concentration a hidden risk for Indian economy

GDP mis-estimation charge raises a credibility problem

There is also a deeper institutional point. India GDP mis-estimation controversy was never just about one number. It was about credibility. A national accounts system must command enough confidence that governments, investors, businesses and the Reserve Bank of India can use it without constant caveats. Once that confidence is weakened, policy itself becomes noisier. Monetary policy may be tighter than warranted if real activity is weaker than reported. Fiscal strategy may look more prudent than it is if the denominator is overstated. Corporate boards may misread demand conditions. A statistical system is not a technical sideshow. It is part of the economic constitution.

The official response in 2026 suggests that the criticism was not entirely misplaced. The government’s new GDP series with base year 2022-23 explicitly says it is incorporating improved sources such as ASUSE, PLFS, GST and PFMS, and improving the measurement of the informal and services sectors. MoSPI’s own explanatory material says regular surveys will now allow direct annual estimates for the unincorporated sector instead of leaning on old survey benchmarks and related indicators. In plain language, the system has moved toward exactly the terrain where critics had asked it to move. That does not prove the Peterson Institute paper right on every number. But it does amount to an official acknowledgement that the previous framework had important limitations.

The sensible conclusion, then, is neither triumphalist nor cynical. India probably did mis-estimate GDP over a long stretch, especially after 2011. The mis-estimation likely exaggerated the resilience of the economy after a sequence of shocks that bore down hardest on the informal sector. The Peterson Institute paper deserves to be read seriously because it offers a coherent explanation for a puzzle many had noticed but few had quantified well. Yet its own reconstructed series should be seen as a challenge to the old numbers, not the last word on them.

What should happen next is straightforward. MoSPI should publish a transparent back series under the new methodology, release detailed sector-wise sources and assumptions, and invite open scrutiny from statisticians, academic economists and former national accounts practitioners. India does not need a defensive debate on whether criticism is patriotic. It needs a better statistical compact. Fast-growing economies can survive bad headlines. They should not have to survive doubtful measurement.