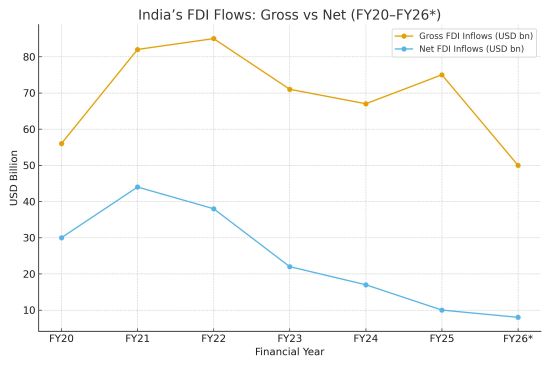

India once stood out in global capital markets as a major emerging economy offering both political stability and robust growth. Foreign direct investment reflected that confidence. Total FDI inflows peaked at $84.84 billion in 2021–22, boosted by years of low global interest rates, the China-plus-one realignment, and a favourable domestic reform narrative. The cycle has now turned. Chief Economic Adviser V Anantha Nageswaran recently warned that India’s investment appeal can no longer be taken for granted. Gross inflows remain healthy, but the more critical measure—net FDI, or capital that stays and expands within the economy—has weakened significantly.

The latest RBI data underline the shift. Gross FDI inflows into India rose 16.1% year-on-year to $50.36 billion in H1 FY26. Yet net inflows fell to $7.64 billion once repatriation and rising outward investment by Indian firms are factored in. This divergence captures an important point: capital is coming in, but much of it is also going out. Developed economies have raised interest rates sharply over the past three years, drawing capital back toward safer assets.

The IMF has noted that global borrowing costs are at their highest levels in over a decade, reducing the risk appetite for emerging markets. Indian companies, meanwhile, are investing more abroad to diversify supply chains, hedge currency risk, and access new markets. These structural outflows dampen the domestic availability of long-term capital.

READ I Deregulation drive: Can states deliver the next big reform?

The quality of FDI inflows matters

Headline numbers are only part of the story. The composition of FDI inflows has shifted toward mergers and acquisitions rather than greenfield projects. Services continue to dominate inflows, while manufacturing has not yet gained the scale needed to transform the production base. Greenfield FDI—typically associated with technology transfer, job creation, and export potential—has been subdued over the past three years, even as global supply chains are being reconfigured. The distinction between inflows that merely change ownership and those that create new productive capacity will matter for India’s growth model.

It is also essential to recognise the size of the lever India is pulling. FDI inflows accounts for a small share of gross fixed capital formation, which is still overwhelmingly driven by domestic savings. Foreign investors play a catalytic role by bringing technology, integrating local firms with global value chains, and improving productivity. However, even in optimistic scenarios, FDI inflows cannot be expected to replace the need for strong domestic investment cycles. A credible strategy must therefore combine external capital with a stable domestic investment environment.

Investment decisions increasingly depend on sub-national competitiveness. A handful of states—Maharashtra, Karnataka, Gujarat, Tamil Nadu, and Telangana—have accounted for a large share of India’s inflows over the past decade. Differences in logistics costs, power reliability, urban governance, land acquisition processes, and contract enforcement shape investor decisions more than headline national reforms. As India seeks to expand its manufacturing base, state-level regulatory consistency and administrative capacity will be as important as Union-level policies.

Manufacturing push and the need for reform

India’s long-term strategy places manufacturing at the core of economic transformation. The sector currently accounts for 16–17% of GDP, according to the National Statistical Office, with an ambition to raise that share to 25% by 2030. The government expects FDI inflows to play a central role in this transition.

Between 2014 and 2024, manufacturing attracted $165.1 billion in equity inflows—a 69% increase over the previous decade, based on DPIIT data. Yet the path to a larger manufacturing base will require more than isolated investment surges. Logistics, labour-market readiness, regulatory clarity, and infrastructure gaps remain persistent constraints, despite significant progress in freight corridors, ports, and digital systems.

Policy credibility and treaty architecture

The ease-of-doing-business narrative must now be complemented by policy predictability. Foreign investors continue to flag concerns over tariff volatility, frequent regulatory changes, and patchy contract enforcement. India’s network of bilateral investment treaties (BITs) has also thinned after most agreements were terminated in 2016–17, reducing legal protection for long-term investors. The government is reviewing the BIT framework, but a credible mechanism for dispute resolution and investment protection will be essential as global capital becomes more risk-sensitive.

India is now competing not just with emerging-market peers but with a wider spectrum of investment destinations. Vietnam’s FDI inflows-to-GDP ratio remains more than double India’s, according to World Bank data, reflecting its integration into electronics supply chains. Mexico has seen record inflows amid near-shoring to North America. These comparisons matter because many investors assessing India evaluate it alongside these alternatives. India remains attractive on scale, demographics, and political stability, but will need sharper reforms to match the agility of smaller export-driven economies.

Climate, energy, and ESG filters

A new layer shaping capital flows is the rise of ESG and climate-linked investment norms. Global firms increasingly evaluate host countries on carbon policy, renewable-energy availability, and labour and environmental standards. The EU’s Carbon Border Adjustment Mechanism (CBAM) and similar initiatives will influence where companies choose to build new production facilities.

India’s success in expanding renewable capacity and reducing logistics emissions will therefore be pivotal in deciding the future geography of global supply chains.

India could still cross the symbolic $100-billion gross FDI inflows mark in FY26. But the more relevant metric remains net inflows, which reflect the durability of investor commitment. The message from recent data is unambiguous: global conditions are no longer aligned in India’s favour, and domestic policy must do more of the heavy lifting.

A targeted FDI regime, credible regulatory institutions, deeper state-level reforms, and infrastructure upgrades will be essential to attract long-horizon investors who can support India’s manufacturing ambitions.

Gross inflows can create headlines. Only net, productive, greenfield investment can transform the economy. The next phase of India’s growth will depend on turning short-term opportunity into long-term capital that stays, scales, and strengthens the country’s industrial foundations.