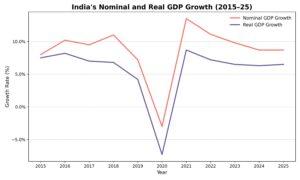

India’s 8.2% real GDP growth in Q2 FY26 has renewed optimism about the economy’s momentum. But the celebration may be premature. Nominal GDP growth has slipped into single digits, well below the Union Budget’s 10.1% projection, and the GDP deflator—the broadest measure of economy-wide price changes—has fallen to a 24-quarter low. The gap between strong real output and weak nominal income is no longer a statistical curiosity; it is a macroeconomic signal that policymakers can ignore only at their peril.

Nominal GDP measures output at current prices while real GDP adjusts for inflation. The GDP deflator, derived by dividing nominal GDP by real GDP, captures how prices move across the entire economy. When inflation is steady, nominal growth is expected to outpace real growth. A falling deflator reverses this relationship by inflating real output on paper while nominal income struggles to keep pace. That is precisely what the current data show: weak price pressures and subdued demand are making the economy look far more robust in real terms than it feels in income terms.

READ | Why FDI inflows are faltering — and how policy must respond

GDP deflator: Which sectors are pulling down growth

A closer look reveals the sources of the deflator’s decline. The Wholesale Price Index has recorded extended deflation in metals, chemicals, textiles, fertilisers, and petroleum-linked industries. The steep fall in global commodity prices after the Ukraine conflict has sharply reduced pricing power across manufacturing. Agriculture has added to the drag because farm-gate prices have often softened even as retail food inflation remained elevated. Services inflation has remained stable but not strong enough to counter the overall weakness. The sharp fall in the deflator is therefore neither random nor mysterious; it reflects a broad-based stagnation in prices.

Nominal GDP growth shapes both private incomes and public finances. Companies rely on pricing power to maintain margins; without it, profits shrink even when volumes rise. Government revenues behave similarly. GST collections, corporate tax receipts, and income tax revenues depend far more on nominal income growth than on real GDP. A prolonged soft patch in nominal GDP weighs directly on tax buoyancy. This is happening at a time when the government has committed to higher public investment and a faster pace of fiscal consolidation, making the nominal slowdown a structural challenge rather than an accounting anomaly.

Impact on debt ratios and fiscal credibility

The implications extend into fiscal sustainability. India’s general government debt stands at about 81% of GDP, according to the IMF. When nominal GDP grows slowly, the denominator of the debt ratio expands too slowly to reduce the burden. The fiscal deficit ratio also appears worse when nominal GDP remains subdued. A weak deflator therefore complicates the medium-term fiscal strategy and forces either more aggressive revenue mobilisation or sharper spending cuts—both difficult in an election-cycle environment. This risk is not adequately recognised in public debate but is central to macroeconomic credibility.

State finances are even more sensitive to nominal growth than the Centre’s. States account for nearly 70% of India’s public capital expenditure, and their fiscal capacity is tied to nominal GST revenues, state excise, stamp duties and devolved taxes. When nominal GDP stagnates, states experience a squeeze on fiscal space. The result is often delayed infrastructure spending, stalled public-investment pipelines, and a weakening of the broader investment cycle. India’s growth model relies heavily on state-level capex, making weak nominal GDP a constraint on the federal structure as a whole.

The consumption and wage paradox

There is also a household-level contradiction. If real GDP rises sharply but nominal incomes do not keep pace, wage growth stagnates. India’s private consumption share in GDP has already fallen below pre-pandemic levels. Weak nominal wages play a significant role in this trend, limiting the ability of households to support sustained domestic demand. This disconnect between measured output and lived economic experience lies at the heart of India’s uneven recovery and deserves policy attention beyond statistical debates.

India’s divergence between real and nominal GDP is not an isolated phenomenon. Global disinflation, the correction in commodity markets, and tightening financial conditions have pushed down nominal growth across several Asian economies. The IMF’s World Economic Outlook notes similar patterns in countries experiencing post-pandemic normalisation. Recognising this context is important for interpreting India’s data. The issue is not merely an artefact of domestic methodology but also a reflection of international price dynamics.

Is real growth being overstated?

A persistently weak deflator raises a legitimate question: is India experiencing a genuine productivity surge or are statistical effects exaggerating real growth? The debate is not new. India’s national accounts methodology, especially in manufacturing and the informal sector, has faced scrutiny for years. MOSPI’s proposed revision of the GDP base year and modernisation of deflation methods may address some concerns. Until then, the credibility of real GDP numbers will remain closely tied to the reliability of the deflator that underpins them.

A low deflator may appear to create space for monetary easing, and some economists argue that real interest rates have stayed too high. But weak nominal GDP complicates the decision. Lower policy rates cannot, by themselves, restore pricing power or lift revenue growth. More importantly, if the deflator misrepresents underlying price conditions, the RBI’s assessment of the output gap, inflation trajectory and policy transmission may become less accurate. Monetary policy relies on trustworthy indicators; a flawed deflator weakens that foundation.

India has invested considerably in improving its statistical systems through base-year revisions, new surveys and digital-era data. But unless the deflator becomes more stable and better aligned with current economic patterns, the credibility of headline growth numbers will continue to face questions. Growth needs a clear mirror, and the deflator is central to that clarity.

India’s real GDP figures may continue to draw attention, but the weakness in nominal growth demands greater scrutiny. A fragile deflator distorts the picture of economic health, depresses revenues, strains fiscal ratios and restricts the ability of states and firms to invest. National accounts must evolve to provide a more accurate reflection of economic conditions. Strengthening the deflator, updating base years and improving sectoral price measurement are essential steps toward restoring clarity. Until then, India’s headline growth figures must be read not as a sign of unambiguous strength but as data requiring careful interpretation.