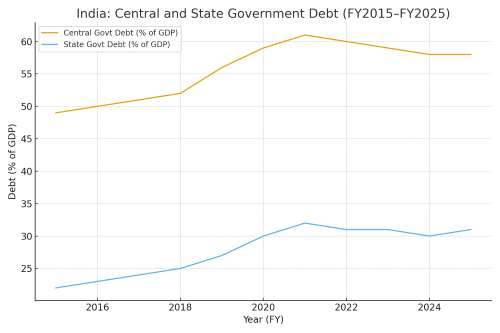

India’s fiscal federalism is entering a new phase as the Union government steadily expands the use of 50-year, interest-free loans to states for capital expenditure — a facility first introduced in the Union Budget and strengthened through new allocations over the year. The latest sanctions, amounting to about ₹3.6 lakh crore, confirm that this form of central support has become a structural feature of the fiscal regime rather than a one-time intervention. The scheme promises fresh resources for infrastructure at a time when most states face shrinking fiscal space and rising expenditure commitments.

Yet it also raises deeper questions about the long-term balance of power between the Centre and the states. These loans help states invest without adding interest burdens, but they also entrench a pattern of dependency that may shape future bargaining within the federal system. As central assistance becomes more closely tied to reform milestones and conditionality, India must evaluate what this trend means for autonomy, accountability, and the sustainability of state finances. The challenge is not only to accelerate capital formation today but to preserve a healthy federal architecture for the decades ahead.

READ I Can India have high growth and low deficit?

Capital expenditure as the new growth anchor

The government has placed capital expenditure at the centre of its growth strategy. Capex tends to have a higher multiplier effect than routine spending, as noted in an RBI study. It creates jobs in construction, boosts demand for raw materials, and builds productive assets. Yet many states have struggled to maintain investment levels. Their revenues lag their spending commitments. GST compensation ended in 2022. Borrowing limits have tightened. As a result, several states now depend heavily on centrally sponsored schemes or special assistance to fund new projects.

The Union government sees this gap as a risk. If states cut back capex, national growth could slow. The 50-year interest-free loans are meant to counter that by nudging states to invest even when their own finances are weak. The amounts are sizeable: in FY25, the Union Budget allocated ₹1.3 lakh crore under this window, in addition to earlier tranches. This makes the scheme one of the biggest drivers of public investment in the country.

But the model also signals a shift. States remain responsible for executing most infrastructure projects, yet their financial autonomy to design them is narrowing. This dependence sits uneasily with the principles of fiscal federalism, which emphasise devolution rather than central direction.

Fiscal federalism and distorted incentives

The scheme’s design raises an important question: do long-term, interest-free loans improve discipline or weaken it? On one hand, the loans increase states’ ability to invest without fuelling debt-service pressures. That helps poorer states, which struggle with weak revenues and limited market access. On the other hand, easy financing can dilute incentives to strengthen local revenue systems, especially property tax and user charges—long-standing weaknesses flagged in several NIPFP analyses.

Richer states may benefit less. Their project pipelines are larger, but they often have the capacity to borrow on their own at competitive rates. For them, conditional loans tied to central priorities may not align with local planning. This creates an uneven map of incentives. States with weaker finances become more dependent. States with stronger finances may opt out or comply reluctantly.

The deeper issue is durability. A 50-year loan gives states resources now, but it also creates a long bond with the centre. When these loans mature in the 2070s, the fiscal situation will be different. But the political message—that states need central support to invest—may become entrenched well before then.

Centralisation, conditionality, and governance gaps

The special assistance scheme comes with conditions. States must meet reform milestones on power distribution, urban planning, logistics, or asset monetisation. The centre’s logic is clear: reforms improve efficiency and ensure better returns on capital. But conditionality also increases central oversight of sectors that are constitutionally state subjects.

This brings governance risks. Many states have limited project-execution capacity. They face delays in land acquisition, contractor management, and environmental clearances. Their ability to absorb large volumes of capex remains uneven. A recent IMF paper found that weak administrative capacity reduces the growth impact of public investment. India’s experience echoes this. Past schemes—from the Backward Regions Grant Fund to special plan assistance—show that funds often remained unspent or poorly monitored.

Centre–state coordination is another challenge. The Union government wants faster execution. States want more flexibility and less micromanagement. This friction can slow projects. It can also lead to disputes on accounting, utilisation certificates, and audit requirements.

Global models of fiscal federalism

Other federal systems offer useful lessons. The European Union’s cohesion funds provide grants and loans to poorer regions, but they come with strict monitoring and transparent reporting. The model ensures accountability but remains complex to administer.

China uses a different approach. Its centre provides broad policy direction while provinces raise significant funds through local financing vehicles. This allows rapid infrastructure growth but creates opaque debt risks—problems India would want to avoid.

Brazil sits somewhere between the two. Its federal development bank, BNDES, supports state-level projects but screens them rigorously for fiscal sustainability.

India’s model borrows pieces from each but lacks the institutional architecture that underpins them. If long-term loans become a permanent fixture, India may need an independent body—perhaps an expanded role for the Finance Commission—to evaluate project pipelines, fiscal risks, and outcomes.

Shaping India’s federal future

The most important question is forward-looking. What happens when these loans mature? By then, several generations of elected governments will have come and gone. The repayment obligations, though small each year, may still affect state finances. A prolonged reliance on central loans could discourage states from expanding their own tax bases or undertaking difficult reforms.

More broadly, the scheme resets the architecture of fiscal federalism. Devolution through the Finance Commission was meant to give states untied funds. GST was meant to harmonise taxes. But the rise of tied grants and conditional loans pushes India toward a more centralised model. This may achieve faster infrastructure expansion in the short term, but it risks limiting innovation and accountability at the state level.

India’s growth prospects depend not just on more capital but on stronger, more autonomous states. As Policy Circle has argued in analyses on India’s growth prospects and the hidden burden of compliance in state systems, institutional strength matters as much as money.

The 50-year loans can play a positive role. They support investment at a time when states face fiscal pressure. They also help align national and local priorities. But they should not become substitutes for durable reforms in state finances. Nor should they weaken fiscal autonomy.

A better balance is possible. The centre can continue to support capex, but it should also set clear sunset clauses, strengthen transparency, and reward states that improve their own revenue systems. India needs sustained investment. It also needs strong, independent states. The long-term loan scheme should empower them, not bind them.