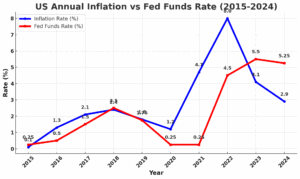

Late Wednesday in Washington, the Federal Open Market Committee chose the path of least regret: it left the federal funds target range unmoved at 4.25-4.50%—its sixth straight hold since January. To some, that may look like timidity. Yet seasoned central bankers know that monetary policy is a waiting game: better to err on the side of caution than to tighten prematurely or ease recklessly. The decision reflects a calculus that inflation risks still outweigh the growth slowdown already visible in housing, retail sales and hiring.

The most potent variable in the Fed’s equation is not macroeconomic at all but political: President Donald Trump’s Liberation Day tariff barrage. After years of skirmishes, the White House has fired a broadside—levies that now touch everything from Korean semiconductors to German machine tools. Fed chair Jerome Powell admitted at his press conference that policymakers “have to learn more about tariffs” before deciding how to react.

READ I How India’s migrant labour struggles during a crisis

A pause, not a pivot

The dilemma is classic. Tariffs are, in effect, taxes on imported inputs. If businesses absorb the hit, margins shrink and investment stalls; if they pass it on, consumer prices rise. Most company surveys suggest the latter. “Many, many firms expect to put all or some of the tariff cost through to the next person in the chain,” Powell warned. That is why the FOMC’s June projections nudged 2025 inflation up to 3%, even as growth expectations fell.

A central bank that has spent three years coaxing inflation down from 8% cannot risk a fresh updraft. Nor can it justify a cut until it knows whether tariff-driven price spikes are transient or sticky. Hence the hold.

Wars and the price of oil

Tariffs are not the only supply shock stalking the Fed. The Iran–Israel conflict has already lifted Brent crude into the mid-$90s, and every dollar added at the pump fans headline inflation. Powell drew a parallel with the 1970s but was quick to note that “the US economy is far less dependent on foreign oil” today. True—yet the psychological transmission mechanism remains. Rising fuel bills seep into freight rates, airfares and food prices long before statisticians notice.

Practically, the Fed cannot hike to suppress an oil shock; that would crash demand without creating a single new barrel. Equally, it cannot ease while price expectations are vulnerable. The prudent course is to bide time, monitor futures curves, and remind markets that one-off energy bursts usually fade. In other words: another reason to sit tight.

Labour market: Breathing room, not alarm

Critics of the hold point to cooling payroll growth and falling housing starts as evidence that policy is too tight. The FOMC, however, believes the labour market still enjoys a cushion of resilience. Unemployment stands at 4.2%—above the 3.5% lows of 2023 but below the level historically associated with recession. Wage growth has slowed but remains above 3.5%, implying that real incomes are stabilising as inflation ebbs.

Here the Fed has learnt from its pandemic mis-step. Tightening too soon risks snuffing out gains for marginal workers; easing too soon risks rekindling inflation and requiring harsher medicine later. Powell’s colleagues therefore signalled only two quarter-point cuts this year, and even those are conditional. Eight of nineteen participants now foresee no cuts at all in 2025—a hawkish tilt that underscores the Fed’s inflation first mantra.

Fed independence under fire

Every Fed meeting now doubles as a test of institutional autonomy. President Trump has been anything but subtle, demanding “at least 100 basis points” of relief and berating Powell for “economic sabotage”. The Chair’s reply was measured but firm: “We will make decisions based on the data and our dual mandate—nothing else.” Markets cheered the assertion of independence even as they marked up Treasury yields; political interference is inflationary in itself because it undermines credibility.

Thinktanks from Brookings to Peterson have warned that any hint of capitulation would de-anchor expectations and raise the neutral rate—forcing the Fed to run policy tighter for longer. By declining to oblige Pennsylvania Avenue, the Committee has preserved its most valuable asset: trust.

Waiting for the data—and July 8

The calendar now rules. Trump’s self-imposed 8 July deadline to finalise bilateral trade deals looms large; so does the possibility that he will extend it to keep talks alive.¹¹ If tariffs broaden or deepen, the Fed’s September meeting could look very different; if they are rolled back, the door to cuts will open. Likewise, if the Israeli-Iranian confrontation escalates into a regional oil shock, the Fed may have to stomach a higher inflation path for longer.

In the meantime, the FOMC Committee will watch three dashboards:

- Core PCE inflation—especially goods prices, which Powell expects to “move up a bit” this summer.

- Labour-market slack—signs that rising joblessness is cooling demand rather than supply.

- Financial conditions—credit-card delinquencies and small-business lending spreads, now edging higher.

Should these indicators worsen in tandem, a “bad-news cut” becomes plausible. Until then, the balance of risks argues for patience.

Lessons for India—and beyond

What does an American rate hold mean for the rest of us? For India, a steady Fed funds rate keeps global liquidity in suspended animation. The rupee enjoys breathing space; yet volatility in oil and food imports may still feed domestic inflation. The Reserve Bank of India, which paused earlier this month, will welcome the reprieve but cannot assume it lasts.

Globally, the Fed’s posture is a reminder that the golden age of cheap money is over. Fiscal authorities who borrowed heavily during zero-rate days must now confront refinancing at 4 per cent plus. Emerging-market policymakers, addicted to inflows, must rediscover the virtues of structural reform. And politicians everywhere might reflect on the perils of conflating trade wars with macro-stability.

Holding the rate steady is not indecision; it is informed restraint. Confronted with tariff fog, Middle-East fire, and a labour market that is easing but not collapsing, the Fed has chosen to stay on the ridge line—ready to advance or retreat as the terrain clears. In doing so, it mirrors the advice long given to Indian policymakers: move only when you must, move decisively when you do, and never confuse noise for signal.

For Jerome Powell, the coming months will test that doctrine. For the rest of us, the June hold is a lesson in the art of central-bank statecraft: sometimes the boldest act is to do nothing at all.