When Nirmala Sitharaman rises to present the Union Budget 2026, she will do so under the comfort of strong headline growth and the discomfort of a fiscal balance sheet that offers little room for manoeuvre. India remains the fastest-growing major economy. Yet the Budget arithmetic behind that claim is tightening, not easing. The challenge before the finance minister is not to announce ambition, but to reconcile competing pressures that have been postponed rather than resolved.

The government’s public optimism rests largely on real GDP growth. Budget arithmetic does not. Nominal GDP growth, the base on which revenues are calculated, has slowed sharply. The First Advance Estimates place nominal growth for 2025–26 at about 8%, far below the 10%-plus assumptions that underpinned earlier fiscal plans.

This matters because expenditure commitments are fixed in rupee terms, while revenues scale with nominal expansion. Lower nominal growth compresses fiscal space even when real output looks healthy. The result is a Budget that must be framed on conservative revenue assumptions, limiting the scope for either new spending or meaningful tax relief.

READ I Budget 2026 must choose productivity over populism

Tax buoyancy has broken down

The second constraint is weaker-than-expected tax buoyancy. Gross tax revenues in the current year have grown more slowly than nominal GDP, pushing buoyancy well below the level assumed at the start of the fiscal year. This shortfall has been masked by higher dividends from the central bank and public sector enterprises, as well as one-off telecom payments.

These are not repeatable sources of revenue. The underlying problem is that recent tax cuts—both direct and indirect—have reduced elasticity in collections without generating a compensating expansion in the tax base. Budget 2026 will therefore begin with a revenue gap that cannot be bridged through administrative tightening alone.

READ I Budget 2026: Why signals matter more than big announcements

Fiscal discipline is market-enforced

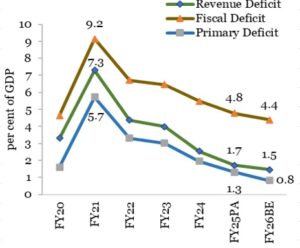

Unlike earlier years, the finance minister’s room for fiscal accommodation is constrained not by political preference but by market scrutiny. The fiscal consolidation path has delivered credibility, stabilised bond yields, and supported a sovereign rating upgrade. That credibility now needs to be preserved.

With debt redemption of roughly ₹5.5 trillion due in FY27 and gross borrowings expected to rise above ₹16 trillion, debt management will dominate Budget calculations. Any perception of slippage risks pushing up yields at a time when state borrowings are also rising. The shift from deficit targeting to debt reduction narrows flexibility further, not less.

READ I Economic Survey 2025-26 flags rising state-level fiscal risk

Capital expenditure: Ceiling, not lever

Public capital expenditure has been the government’s primary macro lever since the pandemic. That lever is close to its ceiling. Infrastructure outlays are expected to remain around 3.1–3.2% of GDP, with little room for a step-up once defence requirements and legacy commitments are factored in.

The political economy is awkward. Capex must be maintained to signal continuity, but it can no longer expand fast enough to offset private sector hesitation. This leaves the government defending a large spending number that is necessary but no longer sufficient.

Private investment still lacks conviction

The more uncomfortable reality is that private corporate investment has not responded as hoped. The government’s initiatives such as corporate tax cuts, production-linked incentives, infrastructure build-out, and consumption-side relief have failed to kick-start a broad-based investment cycle.

Domestic corporates are cautious amid uneven demand and uncertain global conditions. Foreign investors have turned net sellers, reflecting stretched valuations, US tax threats, and concerns over earnings momentum. Budget 2026 must address investment sentiment without the help of any fiscal tool.

Consumption support has run its course

The consumption-driven growth delivered through tax relief in recent years has reached its limit. Further cuts would deepen the revenue hole without guaranteeing a durable demand revival. At the same time, the recovery in consumption remains uneven, creating pressure to protect subsidies and social spending.

This trade-off is central to the Budget dilemma. Cutting welfare risks political and economic backlash. Expanding it risks breaching fiscal targets. The space to finesse this balance is narrow.

Federal transfers and pay pressures loom

Two uncertainties hang over the fiscal math. The first is the forthcoming recommendations of the Sixteenth Finance Commission, which could alter the centre-state revenue split. The second is the prospect of higher salary outgoes for government employees.

Neither is within the finance minister’s control, yet both must be provisioned for. Budget 2026 will therefore be framed under contingent liabilities that limit discretionary ambition.

Budget 2026: Reform without spending

Stripped of fiscal headroom, the Budget is likely to lean heavily on regulatory and structural reform. Easing foreign investment rules in defence, labour law implementation, and sector-specific liberalisation may feature prominently. These measures are necessary, but their payoff is gradual and uncertain.

That is the underlying tension. The Budget must reassure markets in the short term while betting on reforms that work over the long term. It must do so without new money.

Budget 2026 is less a statement of intent than a test of credibility. Strong growth numbers provide political cover, but they do not solve the fiscal arithmetic. The task before Nirmala Sitharaman is to present numbers that are conservative enough to be believed, disciplined enough to satisfy markets, and flexible enough to keep the growth narrative intact.

In that sense, this Budget is harder than those delivered in leaner years. The constraints are subtler, the expectations higher, and the margin for error smaller.