GST 2.0 reforms: When India rolled out the Goods and Services Tax in 2017, it promised a unified market and simplified taxation. Eight years later, the launch of GST 2.0 signals a course correction. The new regime introduces auto-approved registration within three days, faster refunds, and AI-enabled digital audit trails. These are ambitious steps aimed at cleaning up compliance bottlenecks and restoring taxpayer confidence. Yet the key question remains: Can GST 2.0 reforms correct the structural weaknesses that hampered India’s indirect tax regime, and finally deliver the combination of simplicity and buoyant revenues the economy needs?

GST 1.0 unified India’s fragmented indirect tax regime, subsuming excise, VAT, and service tax into one structure. But the implementation exposed deep operational cracks. Compliance was neither simple nor uniform. Businesses faced multiple filings — up to 37 returns a year — and struggled with invoice mismatches between suppliers and buyers. Refund delays often froze working capital, especially for exporters and MSMEs.

READ I Unified labour database: Efficiency gain or surveillance risk?

Tracking the legacy of GST 2.0 reforms

Dependence on the GST Network (GSTN) added another layer of fragility. Frequent portal glitches disrupted filing deadlines, while several states complained of incomplete data integration between their systems and the Union government’s. A 2023 CAG audit found that nearly 15% of refund claims faced delays exceeding 60 days due to software inconsistencies.

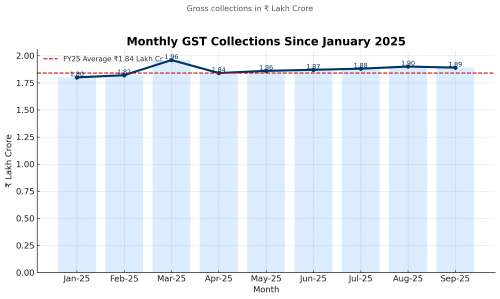

Revenue performance has been mixed. While monthly GST collections crossed ₹2 lakh crore in April 2024 — a record high — experts caution that buoyancy has plateaued. Fake invoicing and under-reporting remain endemic. Between 2018 and 2024, enforcement agencies detected fraudulent input tax credit (ITC) claims worth over ₹1.8 lakh crore. These leakages offset much of the efficiency gains the reform was supposed to deliver.

For MSMEs, GST’s promise of simplicity translated into higher compliance costs. Constant policy tweaks — 375 notifications in the first three years alone — sowed confusion over exemptions and filing norms. According to a FISME survey, compliance costs for small firms rose by nearly 22% compared with the pre-GST era. Many resorted to informal transactions to avoid procedural complexity.

Finally, the institutional structure suffered from imbalance. The GST Council, though designed as a model of cooperative federalism, lacked an independent secretariat. This limited its ability to enforce uniform standards or resolve inter-state disputes, such as disagreements over the compensation cess mechanism. What emerged was not a “One Nation, One Tax” system but a patchwork of divergent interpretations.

GST 2.0 reforms: Registration process gets an upgrade

GST 2.0 reforms promise to tackle these inefficiencies through automation and data intelligence. The auto-approval of registrations within three days seeks to reduce bureaucratic discretion. Real-time analytics and AI-driven fraud detection aim to close loopholes in input tax credits, a key source of revenue leakage.

The rollout of e-invoicing for all businesses above ₹5 crore turnover is another milestone. It creates a unified digital trail from supplier to buyer, helping verify credits and reduce human errors. Similarly, the push for a unified compliance portal and harmonised state portals should, in theory, end the fragmentation between central and state systems. Filing frequencies are expected to drop, cutting compliance time for small businesses.

These changes look promising on paper, but they risk being cosmetic if governance remains reactive. India has often mistaken technology for reform. Without institutional clarity, faster registration could simply automate earlier inefficiencies. AI-based scrutiny can detect fraud but also overwhelm taxpayers with automated notices. Real simplification will come not from algorithms but from stable rules and transparent communication.

The challenge is to ensure that GST 2.0 is not just GSTN 2.0 — a platform upgrade — but a re-engineering of policy and accountability. The government’s success will depend on whether it can match digital ambition with administrative discipline.

Learning from global GST systems

Global experience shows that simplicity and trust, not overregulation, drive compliance.

Singapore’s GST, for example, operates with a single 9% rate and minimal exemptions. Its digital-first model allows instant invoice matching and refunds within days. This simplicity keeps compliance costs below 1% of revenue, compared with nearly 5% for Indian firms.

New Zealand’s VAT system is often hailed as the gold standard — one rate, no exemptions, and complete centralisation. Its transparent administration and predictable refund cycles have helped maintain voluntary compliance at 98%.

Australia, a federal system like India, offers an even closer comparison. Its inter-governmental coordination mechanism ensures that states participate in GST design and enforcement. A dedicated GST Distribution Commission transparently allocates revenues based on formulae that all parties accept.

Finally, the European Union’s VAT framework shows the power of digital integration. Through the “One Stop Shop” mechanism, cross-border digital sellers can register and remit taxes centrally, with revenue distributed automatically across member states. India’s e-commerce sector, which has long grappled with inconsistent interstate taxation, could benefit from adopting similar principles.

The takeaway is clear: successful VAT systems are built not on layers of compliance but on clarity and consistency. For India, the lessons lie in reducing exemptions, stabilising rates, and institutionalising fiscal transparency.

Need for predictable policy

For GST 2.0 reforms to truly succeed, India must focus as much on institutions as on interfaces.

First, the creation of an independent GST Council secretariat is essential. It should have analytical capacity to monitor compliance trends, audit system performance, and propose evidence-based rate revisions. This autonomy can depoliticise rate-setting and strengthen cooperative federalism.

Second, rationalising the rate structure remains the most pressing task. The current four-tier system (5%, 12%, 18%, 28%) complicates classification and invites lobbying. Moving toward three slabs — essentials, standard, and luxury — will make compliance and communication easier while maintaining revenue neutrality.

Third, India needs a GST Ombudsman. Many taxpayer grievances — from technical glitches to refund disputes — could be resolved through an independent mediation mechanism instead of litigation.

Fourth, policymakers must recognise that technology is only as good as the user. India’s 63 million MSMEs need digital literacy programmes and advisory support to navigate new systems. Integrating GST compliance modules into Udyam registration and fintech tools could ease the transition.

Fifth, predictability matters as much as simplicity. The idea of a quarterly “policy freeze” window, during which no major notifications or changes are issued, can help stabilise compliance. Businesses will then plan cash flows and filings without fear of surprise amendments.

Finally, trust must replace fear. Consistent policy, swift refunds, and transparent adjudication can expand the tax base more effectively than punitive enforcement. As the OECD’s tax policy review notes, predictability yields a fiscal dividend by encouraging voluntary compliance and investment.

GST 2.0 reforms offer a chance to redeem a transformative reform that stumbled under its own complexity. India cannot afford to treat this as another technology upgrade. The goal should be governance simplification — fewer rates, fewer filings, and fewer surprises.

If GST 1.0 taught India the perils of overengineering, GST 2.0 must embody the virtues of clarity and trust. A transparent, predictable, and MSME-friendly system can deliver what no algorithm can: genuine compliance and sustainable revenue growth. The reform’s success will depend not on how smart the software becomes, but on how fair and stable the system feels to those who use it.