The first e-commerce transaction was made on August 11, 1994 when a compact disc of Grammy award winner Ten Summoner’s Tales by English rock musician Sting was purchased over the Internet for $12.48 by Phil Brandenberger using his Mastercard. What followed in the subsequent years was an overall reshaping of global trade practices. Taking advantage of the internet penetration and digitalisation of the financial system, companies such as eBay, Amazon and Alibaba gradually changed the way organisations do business and people do shopping. In the last 25 years, e-commerce has travelled a long way to reach $3.5 trillion in 2019, accounting for 14.1% of all retail sales worldwide. This trend is poised to touch $4.88 trillion by 2021, and its share in global retail trade will cross 20% with the extra push due to the Covid-19 pandemic as consumers shun travelling to shops to avoid getting infected.

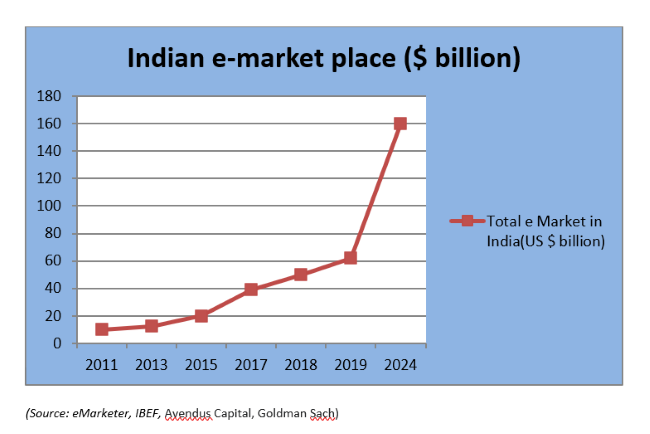

Based on the parties involved in the transactions, the e-commerce is categorised as (i) business-to-business (B2B), (ii) business-to-customer (B2C), (iii) customer-to-business (C2B), (iv) government to business (G2B), (v) consumer to government (C2G), and (vi) customer-to-customer (C2C). However, 80% of the time, it is either B2C or B2B modes. In India, the e-commerce industry is expected to reach $1.1 trillion by 2020. However, the share of online transactions in 2019 was just 4.7% of the total retail business in India, and thus, a vast market is untapped for the online transactions. A battle is on for capturing a major share of the Indian B2C e-commerce market among global giants in the sector – global leader Amazon and WalMart-led Flipkart. Entry of Mukesh Ambani’s Reliance Jio is posing a big challenge to these multinational biggies. Amazon and Flipkart together control close to 63% of the Indian market. Here are some of the largest investments in this space.

READ I India’s retail sector: Overcoming policy and structural challenges

- US-based retailer Wal-Mart, the number one Fortune 500 globally, acquired Flipkart in a $16 billion deal in 2018.

- Facebook acquired a 9.9% stake in Reliance Jio in a $5.7 billion deal to facilitate e-commerce transactions on the JioMart platform.

- Amazon will invest an additional $1 billion taking its total commitment to $6 billion.

- Radhakishan Damani’s DMart is making strides into e-commerce through an entity called Avenue e-commerce, and at the initial stage, will be focusing on Mumbai and Pune.

- Reliance Retail’s deal to acquire Future Group of Big Bazaar fame for $3.4 billion was challenged by Amazon in a Singapore arbitration court which ordered a temporary halt on the acquisition.

- Global retailer Walmart may invest $20-25 billion in the super app of Tata Group as two groups plan to collaborate through Wal-Mart controlled Flipkart.

- Tata Group is reportedly in talks to acquire a majority stake in BigBasket, India’s largest online food and grocery store, for about $1 billion.

- The Confederation of All India Traders (CAIT) launched the logo of a new national e-commerce marketplace BharatEMarket on October 31 to club physical trade with the e-commerce market. The portal proposes to list its 70 million traders and nearly 40,000 trade associations it represents.

Policy and Priorities

READ I Drawing a line: Protection of personal data in a digitised world

The rapid growth of e-commerce has posed a major challenge for policymakers in India in identifying imperfections and imbalances in the market, and to inject necessary regulatory interventions to protect the interests of the public and promote fair practices. In February 2019, the Narendra Modi government brought out a draft policy framework to fill the regulatory gaps in the digital commerce sector. The draft released by DPIIT lists (i) Data storage, processing, protection, privacy, and it’s cross-border migration,(ii) infrastructure development for the digital economy, (iii) consumer protection and level playing field for MSMEs/ small traders, (iv) promote Make in India, (vi) anti-counterfeit measures, and (vii) export promotion, as the main focus areas.

The digitisation of markets has enabled the creation of large amounts of data with the potential to generate significant economic value for consumers and the economy as a whole. But, as consumer data flows, the risks to data privacy increase too. As such, the issue of data protection has been covered extensively under the draft policy, although the issue is not specific to e-commerce. Expectedly, the electronics and IT ministry was quick to introduce The Personal Data Protection Bill, 2019 in the Lok Sabha. The provisions of the bill seem to restrict cross-border transfer of sensitive data and ensuring localisation of data storage. Perhaps, the government believes that increased investment in creating data infrastructure in the country would lead to more jobs within the country.

The FDI policy, which is also administered by DPIIT, permits foreign investment in B2C e-commerce only under the “marketplace model”, and not under the “inventory-based model”. The policy explains that a marketplace e-commerce entity shall not own or exercise control over the goods sold on the platform. Any ownership or control over the goods sold by the market place entity will render the entity an inventory-based business. The restrictions on the inventory-based model are to protect the conventional kirana stores from the cash-rich e-commerce entities. For obvious reasons, CAIT has welcomed the policy as it has helped to create a more favourable market for offline retail stores.

READ I Creating a world class capital goods industry in India

The customers also have more choices for a product within a portal. However, it is to be seen how the policy framework will safeguard the conventional brick and mortar stores from large domestic houses with deep pockets. Some experts feel that instead of prohibiting foreign players from adopting an inventory-based model in India if FDI is permitted subject to a minimum investment by a foreign investor in the development of back-end infrastructure including temperature-sensitive supply chain, and linkages with local players, it may help to modernise the retail market and integrate the traditional “mom-and-pop shops” with the e-commerce market as well.

With the induction of technology in the market, the last-mile delivery can be improved, and also will enable policymakers to counter criticisms by MNCs of depriving them of a level-playing field. Interestingly, even the CAIT has been complaining only against the foreign-owned e-commerce majors like Amazon and Walmart-Flipkart, accusing them of violation of FDI policy, and requested the government to set up a regulatory body for e-commerce for monitoring the business.

Digital Infrastructure support

In India, backed by the 3G, 4G services, and declining data tariffs, internet penetration witnessed substantial growth from 4% in 2007 to 52.08 % in 2019 covering 687.62 million people. One area where India lags is internet speed. Despite initiatives under Digital India, people are still struggling to get good data speed. The recent Speedtest Global Index has ranked India’s mobile internet speeds at 131 out of 138 nations, behind neighbouring nations like Sri Lanka, Nepal, and Pakistan. India’s average mobile download speed is 12.07 mbps, much lower than the global average of 35.26 mbps. Poor Internet speed leads to transaction failure and discourages people from using digital payment methods. A common user of the broadband fails to understand why observed broadband speeds are not consistent with the speed advertised by internet service providers (ISPs). In Germany, the government regulatory agency provides software tools to help users measure connection rates, and if the speeds in 90% of tests do not reach the advertised speeds subscribers can sue the service provider.

READ I Vision 2040: 15 trends that will shape the future of healthcare

The low bandwidth speed in India is the result of the high cost of spectrum, and the ISPs, already under debt, are not able to invest in acquiring more spectrum. With the rise in internet users, the available bandwidth is being shared among the increasing number of users, resulting in low speed. Further, the data consumption on average has increased by 30% in the lockdown period. With the number of internet users expected to reach 829 million by 2021, and anticipated increase in smartphone users/internet subscribers in rural areas (currently around 30%), upgrading the present infrastructure like the deployment of optical fibre, installation of more towers, and rationalisation of spectrum prices have become imperative. The policy must highlight the necessity of improved digital infrastructure for deriving full benefit from a digital economy.

Warehousing and transportation network

From the perspective of a consumer, an efficient e-commerce entity is the one that ensures time-bound delivery of the product purchased online, maintaining agility in the logistics chain. In the increasingly complex urban areas, it means not only quick and flexible transportation, but also localised delivery through smart warehousing, multi-commodity storage facilities, real-time traceability, inventory control using evolving technologies, and offline trader’s network.

In India, the next phase of growth is expected to come from tier II, and smaller towns. Insufficient storage facilities and lack of air and road connectivity for tier II/III cities with metros are considered major bottlenecks in the growth. Inadequate logistics has affected the profitability of the e-retailing industry as it means higher delivery costs. The decision of the finance ministry to grant infrastructure status to the logistics sector, covering cold chain and warehousing facilities is a welcome move, and the e-commerce policy should emphasise the need for attracting investment in logistics through incentives and tax exemptions.

READ I Atmanirbhar Bharat: Some practical steps to boost manufacturing in MSME sector

Payment methods and security concerns

As per a study conducted by consultancy firm Bain and Company, India is the fastest-growing market for online shopping in the world. As regards the major players, Paytm, PhonePe, Google Pay, and others are fighting for a slice of the payment cake. With the entry of WhatsApp in India’s online payment market, its 400 million user base will help the firm capture a significant share in the fast-growing UPI-based payment landscape and offer a tough challenge to current market leaders. The recent estrangement between Google and Paytm over Play Store should be seen in the context of Paytm being a competitor to Google Pay. Among issues that bother online buyers, the safety of online money while transacting is the biggest concern. Consumers are sceptical about the account being hacked, and other security lapses.

Making cyberspace secure is another area that needs to be underlined under the broader policy framework for e-commerce. It is often seen that small businesses ignore such security concerns, and do not go for authentication or certification. Making the certification requirement mandatory for all such platforms should be a priority.

The bottom line

READ I Covid-19: Digital preparedness, strong local government key to economic recovery

E-commerce is contributing to the national economy in a significant manner, and its share in India’s GDP has shown an upward trend from 0.5% in 2011 to 0.9% in 2018. It has offered opportunities to MSMEs and small farmers to sell on marketplaces, and cater to a much larger customer base, thus increasing their outreach, and revenue. Its positive impact on employment scenario will be seen along the complete value chain like logistics, warehousing, ITeS, and also in encouraging entrepreneurship. Increased investment by the large corporations in logistics like transportation including cold chain, packaging, and storage will improve facilities in tier II & III cities developing them as new growth centres. Direct linkages between farmers, processors, and organized retailers, reducing the intermediaries to the extent possible, can enhance farmers’ income.

The Inter-disciplinary nature of e-commerce has been acknowledged under the draft e-commerce policy, and accordingly, various arms of the government will deal with the issues of e-commerce industry as outlined in the draft policy.

The policymakers must ensure that the policy interventions result in stimulating investment flow all along the value chain, triggering higher productivity and efficiency, at the same time protecting the interests of all stakeholders including customers. They should address deficits in infrastructure spending, and create a conducive environment for attracting private investments.

(Krishna Kumar Sinha is an industrial policy and FDI expert based in New Delhi. His last assignment was as an industrial adviser in the department of industrial policy and promotion, DIPP, currently known as DPIIT, under the ministry of commerce and industry of the government of India.)