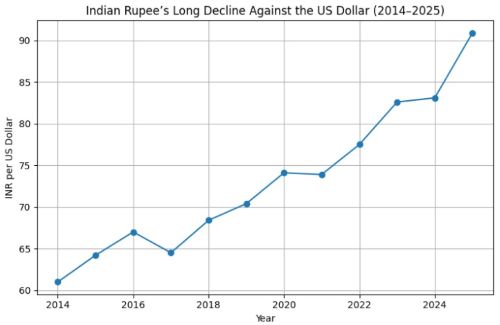

The rupee crossed the 91-per-dollar mark in intraday trade this week, marking its weakest level on record. Over just 10 trading sessions, it has slid from 90 to beyond 91, with losses accelerating in recent days. Portfolio outflows, uncertainty over India–US trade negotiations, and persistent global dollar strength have converged to pressure the currency.

This moment matters because it tests the Reserve Bank of India’s exchange-rate doctrine. For years, the RBI has resisted sharp rupee movements through spot and forward interventions. But the latest episode suggests a shift. With a large short dollar forward position and reduced spot market activity, the central bank appears willing to tolerate a weaker rupee, at least for now.

The argument here is not that depreciation is costless. It is that resisting adjustment carries higher medium-term risks. When a currency is persistently misaligned with fundamentals, defending a nominal level delays correction, distorts incentives, and drains policy credibility. Allowing the rupee to move closer to its real value may now be the more prudent institutional choice.

READ I Rupee depreciation: The currency faces a slow, structural slide

RBI’s evolving intervention strategy

The instinct to defend the rupee at moments of stress is deeply ingrained in policymaking. It is a legacy of scarcity, not of strength. That instinct was understandable when reserves were thin, inflation volatile and external financing fragile. It is less defensible today. Persisting with it risks mistaking comfort for prudence. A central bank that has spent decades building credibility does not need to signal resolve through constant intervention. Markets, after all, are quicker to test conviction than to reward it.

India officially follows a market-determined exchange rate, with RBI intervention aimed at curbing excess volatility rather than defending a fixed level. In practice, however, intervention has often leaned toward smoothing depreciation episodes more aggressively than appreciation phases, creating an implicit floor.

READ I Rupee depreciation: The real drivers of India’s currency fall

That asymmetry is now under strain. RBI’s short dollar forward position — estimated at about $63 billion by October — has shifted intervention away from the spot market. This structure dampens immediate volatility but also reduces the central bank’s ability to counter sustained flow-driven pressure without further tightening rupee liquidity. As the RBI itself has acknowledged in multiple annual reports, large forward books complicate liquidity management and can amplify stress when global conditions turn adverse.

Crucially, the current depreciation is not disorderly. India’s foreign exchange reserves remain above $600 billion, covering more than 10 months of imports, according to RBI data. Inflation has moderated sharply, with CPI inflation easing below 5% in recent readings. The current account deficit, while persistent, has narrowed with import compression, as shown in RBI balance of payments statistics.

In this context, aggressive defence risks confusing stability with rigidity. A currency that cannot adjust to global shocks eventually forces adjustment through growth, credit, or employment — channels far more damaging than price signals in the foreign exchange market.

READ I IMF flags rupee flexibility shift as RBI reduces intervention

Capital flows, trade shocks, currencies

The rupee’s weakness has been driven primarily by capital flows rather than trade fundamentals. Foreign portfolio investors have sold more than $18 billion worth of Indian equities in 2025 so far, according to NSDL data. India has also seen moderation in FDI inflows amid global uncertainty and higher US yields, as reflected in UNCTAD investment reports.

Trade policy uncertainty has compounded these pressures. India remains without a bilateral trade agreement with the United States at a time when tariff barriers are rising. According to WTO trade monitoring reports, global trade growth has slowed sharply, while country specific tariffs have become a more prominent risk factor for exporters. Currency defence cannot offset these structural and geopolitical headwinds.

Attempting to hold the rupee at a preferred level under such conditions merely shifts the burden onto reserves and domestic liquidity. Past emerging-market episodes — from Indonesia in 2013 to Brazil in 2015 — show that defending against capital-driven moves rarely succeeds unless backed by capital controls or sharply higher interest rates. India has rightly avoided both.

A weaker rupee also acts as a partial shock absorber. Export-oriented sectors such as IT and pharmaceuticals have already benefited, with the Nifty IT index rising roughly 14% since late September. More importantly, import compression has improved the trade balance faster than export volumes could have, a dynamic highlighted in World Bank trade elasticity studies.

Real effective exchange rate

The more compelling argument for allowing depreciation lies in valuation. India’s real effective exchange rate (REER) has remained elevated for much of the past decade, reflecting higher domestic inflation relative to trading partners and sustained capital inflows. According to RBI REER indices, the rupee spent extended periods above its long-term average, indicating overvaluation.

Bank of America Global Research estimates that the rupee has already undergone a real depreciation of over 12%. Yet even after this adjustment, it argues that the recent slide reflects cyclical overshooting rather than structural weakness, projecting a return toward 86 per dollar by 2026 as global conditions ease. This assessment aligns with IMF External Sector Reports, which have repeatedly flagged the importance of allowing emerging-market currencies to adjust to inflation differentials over time.

Preventing nominal depreciation in the face of persistent real overvaluation creates a false sense of stability. It subsidises imports, penalises tradables, and encourages external borrowing. Allowing the rupee to move closer to its equilibrium restores price signals across the economy, even if the adjustment is uncomfortable in the short run.

The risk, often cited, is imported inflation. But with global commodity prices subdued and domestic inflation expectations anchored, pass-through remains limited. RBI research papers consistently show that exchange-rate pass-through in India has declined significantly since the 2010s.

Growth, credibility, and institutional trade-off

Currency policy is ultimately about credibility, not cosmetics. The RBI’s primary mandate is price stability, with growth as a secondary objective. Using reserves to defend a particular exchange-rate level when inflation is under control risks diluting that mandate.

Markets appear to recognise this trade-off. Barclays and other global brokerages now expect the RBI to prioritise growth over currency defence, especially as global monetary conditions remain tight. That expectation itself stabilises behaviour, reducing the risk of speculative attacks.

The more serious risk lies in mixed signalling. Intervening episodically without a clear framework can encourage one-way bets, increasing volatility rather than reducing it. By contrast, allowing the rupee to settle within a wider, market-driven band reinforces the RBI’s stated policy stance and preserves institutional consistency.

India’s macro fundamentals remain resilient by emerging-market standards. Growth remains above 6%, public debt is largely rupee-denominated, and external vulnerability indicators remain manageable, as documented in IMF Article IV consultations. A currency that reflects these fundamentals will, over time, command confidence without constant defence.

Letting adjustment work for the rupee

The rupee’s recent slide has understandably unsettled markets. But it does not constitute a crisis. It reflects a confluence of global dollar strength, capital flow reversals, and trade uncertainty—forces beyond the reach of currency intervention.

Attempting to resist this adjustment through aggressive defence would impose higher long-term costs. It would drain reserves, complicate liquidity management, and delay the realignment of relative prices. Allowing the rupee to move closer to its real value, by contrast, preserves policy credibility and enables the economy to absorb external shocks more smoothly.

The RBI’s apparent restraint in recent weeks may therefore be less a retreat and more a recalibration. If inflation remains anchored and financial stability risks contained, the case for tolerance is strong. Over time, as global conditions normalise, a currency aligned with fundamentals will recover without coercion. Stability achieved through adjustment endures longer than stability imposed by defence.