India is trying to sprint at a moment when the world economy has slowed to a careful walk. That contrast will define how far the country can go over the next decade.

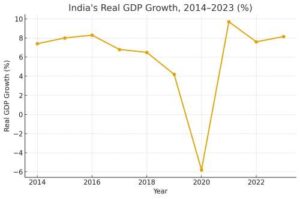

Most forecasters now peg India’s growth at about 6–6.5 % a year. Recent data suggest it can do a little better, helped by policy support and some structural strengths. Yet it is equally clear that the country is not growing anywhere near its potential. The question is why — and what must be done in a world that has lost much of the momentum that powered earlier Asian success stories.

READ I Services inflation now India’s biggest price challenge

Global economic growth slows

Korea, China and other star performers of the late twentieth century benefited from a benign backdrop: robust global growth, expanding trade and rising productivity. That phase is over. Since the mid-1970s, world growth has trended downwards and central banks responded to every dip with lower interest rates. The result has been an economy increasingly driven by debt rather than productivity.

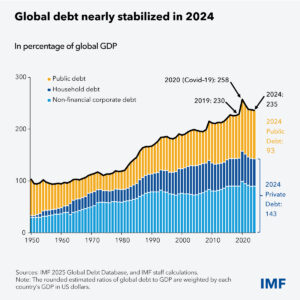

According to the Institute of International Finance (IIF), global debt reached roughly 330% of world GDP in 2023. Meanwhile the International Monetary Fund (IMF) puts total global debt just above 235% of GDP in recent estimates. The discrepancy reflects definitional and data issues, but the broad point holds: debt has surged.

Global trade, once a reliable tailwind, is flat. Data from the World Trade Organisation show that trade in goods and services has hovered around 60% of global GDP for years. Protectionism, tariffs and geopolitical risk now add headwinds. India must build its own momentum in this tougher terrain.

India’s long catch-Up

India’s long-term story is one of delayed catch-up. In the early 1960s, per capita income was about one-fifth of the world average. By the mid-1960s it fell below seven per cent of the world average — India grew, but the world grew faster.

Liberalisation in the early 1990s, the dismantling of the licence raj and gradual trade openings finally changed the slope of the line. Trade openness more than doubled between 1990 and 2012. India’s per capita income relative to the world average has since climbed back to roughly where it was in the early 1960s. That means three decades of reform delivered a regained position, not a leap ahead.

A comparison with the Chinese path is instructive. In the late 1980s China and India were nearer to each other in income per capita; thereafter China leveraged exports and massive investment (including debt) to surge ahead. India has been more cautious, and safer — but equally slower.

Structure, demography and the inequality trap

The structure of India’s economy shows both progress and unfinished business. The agriculture and allied sector now contributes about 17.8 % of GDP. Yet, labour force data show agriculture still employs around 46.1 % of the workforce. This mismatch is a recipe for low productivity, disguised unemployment and stagnant rural incomes.

Premature de-industrialisation, once a risk, appears to be halting. Manufacturing share has stabilised and key government programmes (PLI schemes, logistics upgrades) offer hope. Demography remains a potential asset: since 2018, India’s population growth has fallen below the global average — a trend that can accelerate per capita incomes, provided employment keeps pace. If it does not, the so-called “dividend” becomes a burden.

Much commentary — especially from abroad — focuses on inequality within India. Valid as that is, another gap looms: inequality between countries. Per capita incomes in high-income economies are 30 to 40 times India’s. Closing that gap demands growth well above 6.5 % for many years, not automatic progress.

Debt, credit and the missing bond market

On debt, India occupies an awkward but improving position. General government debt is about 80 % of GDP — not trivial. But as global debt has surged, India’s relative standing has improved. Rating agencies take note.

More interesting is private sector debt. The ratio of household and corporate debt to GDP remains one of the lowest in any large economy. That implies an under-used lever for future growth — if it is used carefully.

Credit from scheduled commercial banks stands at roughly half of GDP and growth has recovered since the clean-up years. But the credit-to-deposit ratio is now above 80 % in many banks. Liquidity, not capital, has become the binding constraint; interest rate cuts alone cannot shift the constraint since lower rates tend to spur deposit outflow.

That is why the corporate bond market has become critical. Outstanding volumes still hover at around 16 % of GDP and secondary market liquidity is weak. In advanced economies bond markets are many multiples of GDP. If India deepens its bond market over the next two decades, it could add one to two percentage points to annual growth without raising systemic risk. For reformers this is the more promising lever, not repeated rate cuts.

Recent fiscal stimuli show that the government is not ignoring cyclical pressures. The rationalisation of GST rates and higher income tax thresholds are mild stimulants in a global climate of weak external demand and rising tariffs. In a country where fewer than 2 % of adults file income tax, raising thresholds may seem modest, but it boosts margins of disposable income.

The tax‐mix is gradually changing. Direct taxes (especially personal income taxes) now absorb a larger share of revenue; customs duties as share of imports have fallen dramatically since the 1990s — even as India imports more. This contradicts the simple narrative of India simply turning protectionist.

Trade opportunity and productivity constraint

Trade is where India’s potential is most clearly under‐exploited. Global trade may be flat as forecast, but India’s share of it remains well below its share of world output. The WTO estimates India accounted for about 1.8 % of global merchandise exports in 2023 and about 4.6 % of commercial services exports — despite a nominal GDP share nearer 7 %. In most of the largest importing markets, Indian exports are still a rounding error; in that sense, India’s export headroom is very large.

India has begun to gain scale in strategic sectors. It is now the world’s second-largest steel producer; in recent years it has become the world’s largest rice exporter. Yet in other areas where it once led — natural rubber is one example — it has allowed itself to become a major importer. Supply-chain shifts (China-plus-one) in electronics, pharmaceuticals and intermediate goods therefore offer a second chance. Whether India seizes it depends on how coherent its trade and industrial policy becomes, and how quickly domestic bottlenecks are addressed.

All these levers — demography, debt, trade — ultimately run up against a hard constraint: labour productivity. On paper, using PPP-adjusted figures, India’s output per worker appears only moderately behind China or Brazil. In practice, competitiveness is judged in nominal terms — what firms pay wages for and what they sell goods for — and on that basis India’s labour productivity gap is far wider. Other emerging economies such as Vietnam are improving productivity faster than India.

Raising productivity will require steady work on basics: reliable power, better transport, efficient urban governance, clearer land and labour rules and stronger investments in human capital. It also means accepting that some concentration of enterprise is inevitable as firms attain global scale. That transition can worsen certain inequality indicators in the short run even as it lifts average incomes.

World needs India’s to grow

Despite wars, tariff hikes and weak global growth, India’s short-term indicators are not flashing red. Manufacturing PMI is near multiyear highs; services output remains positive; capacity utilisation is rising though not yet at levels that trigger a broad-based private capital expenditure boom. On current trends, that cycle looks more likely to begin around 2027 rather than 2026 — delayed, but not derailed.

In other words, India is likely to stay well above the old “Hindu rate” of 3–4 % and probably above 6 % for some time. That is good — but not enough. A world weighed down by debt, demographic headwinds and protectionism will not supply the tailwinds that propelled Korea or China decades ago. India must generate more of its own momentum.

That means building a deeper bond market so long-term investment no longer depends solely on the banking system. It means using trade policy to move up global value chains rather than merely defending the status quo. It means fiscal prudence that leaves room for productive public investment in infrastructure and people. And above all, it means treating productivity — not just scale — as the central objective of economic policy.

If that agenda is pursued with some consistency, India can grow modestly ahead of today’s 6–6.5 % consensus without courting crisis. In a slowing world, the global system still needs a large, reasonably stable source of demand and dynamism. India has the opportunity to play that role. Whether it also narrows the income gap with richer nations will depend on how seriously it treats the hard work of becoming more productive — not just bigger.