India’s banking sector is lending at a faster pace than it is mobilising deposits, pushing the credit-deposit ratio above 80% for the first time in years. RBI data for the fortnight ending October 31 places the credit-deposit ratio at 80.21%, marginally above the central bank’s preferred band of 75–80%. The number itself is not alarming, but the underlying trend is. Credit demand is strong while deposit growth has slowed, revealing a structural funding problem that goes far beyond temporary shifts in interest rates.

Banks now face a widening gap between the money they lend and the money they mobilise. Unless addressed early, this imbalance will tighten liquidity, raise funding costs, and constrain the banking system’s ability to support economic growth.

READ I Core sector stalls in October as energy weakness deepens

The credit-deposit ratio and system liquidity

The credit-deposit ratio measures how much of the money collected as deposits is deployed as loans. A ratio within the 75–80% range reflects a healthy balance: banks are lending efficiently while keeping enough liquidity to meet withdrawals and regulatory requirements. Moving above the upper threshold does not signal immediate distress, but it indicates that banks are pushing the limits of their funding base.

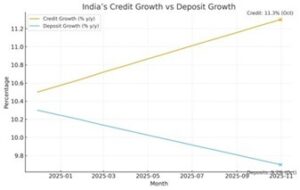

The latest data captures an unmistakable trend. Deposit growth slowed to 9.7% in October from 10.3% in March, while credit growth rose from 11% to 11.3% during the same period. This divergence has appeared at a time when loan demand traditionally strengthens, particularly in the second half of the year. The result is predictable: a system in which lending expands more quickly than the pool of money available to fund it.

Falling household financial savings

Beyond interest-rate movements lies a more important structural issue: India’s household financial savings rate has declined over the past two years, according to RBI and MoSPI estimates. This erosion in savings must be seen as the central explanation for why deposit growth remains weak.

Lower savings have meant that households have less surplus to park in bank accounts or fixed deposits. In such an environment, even if banks increase deposit rates, the response will remain subdued because the underlying saving pool itself has shrunk. This is the most important factor driving the credit-deposit ratio upward, and it poses a long-term challenge to the banking system’s liability base.

Mutual funds and small savings gain

The second major shift is the financialisation of household savings, which has accelerated as returns on market-linked instruments improved. With banks transmitting rate cuts more aggressively on deposits than on loans, fixed deposits have lost their appeal. The weighted average rate on new term deposits has fallen by 106 basis points in the current easing cycle.

As deposits lose ground, money is flowing into mutual funds, money-market schemes, and short-duration debt funds that offer better post-tax returns, especially for urban savers. Small savings schemes, whose government-administered rates have remained unchanged despite falling market yields, have become even more attractive. These instruments provide higher returns with sovereign guarantee — an offer most banks cannot match without denting their margins.

This structural shift in how households save is one of the clearest pressures on the banking system. It drains deposits even as credit expands, making the credit-deposit ratio structurally higher.

UPI has reduced deposit stickiness

Digital payments have changed the dynamics of deposit mobilisation. UPI transactions have grown exponentially, increasing the velocity with which money moves through the system. Households are keeping less idle cash in savings accounts, eroding low-cost CASA deposits, which have traditionally supported bank profitability.

This change is subtle but significant. When digital payments reduce the duration for which deposits remain with banks, CASA balances stagnate or decline. Banks are then forced to rely more on term deposits, which are costlier. As cheap deposits shrink and expensive deposits rise, funding pressures increase. This has a direct bearing on margins and further tightens the credit deposit ratio.

Corporate credit revival adds momentum

Another shift is underway in the credit-demand equation. After years of deleveraging, companies are gradually returning to banks for loans. Capacity utilisation in manufacturing is rising, consumption is stabilising, and the credit mix is moving back towards a healthier balance between retail and corporate loans. This revival, when combined with steady retail borrowing, accelerates overall credit growth and intensifies the need for fresh deposits.

Several banks have already responded by raising interest rates on select deposit products. ICICI Bank’s decision to raise senior citizen deposit rates to 7.2% reflects a broader trend: lenders are now forced to bid harder for deposits despite a soft interest-rate environment.

RBI liquidity support helps, but only temporarily

System liquidity remains comfortable for now. Banks’ reliance on short-term funding remains low, with certificates of deposits accounting for only around 2% of total deposits. The RBI’s phased 100-basis-point cut in the cash reserve ratio has released additional liquidity, easing pressures in the short term. Overnight rates have softened, and liquidity has stayed in surplus for most of the recent months.

However, this comfort may not last. With expectations of another repo rate cut in the December policy meeting, borrowing costs may decline further, stimulating more loan demand. At the same time, lower deposit rates could weaken deposit mobilisation, keeping the CD ratio elevated for longer.

A medium-term funding challenge

A high credit-deposit ratio does not indicate an immediate crisis. But if credit keeps growing faster than deposits, banks will find themselves squeezed on liquidity, margins, and regulatory buffers. The combination of falling household savings, growing preference for market-linked instruments, and digital payments reducing deposit stickiness means this is not just a cyclical imbalance — it is a structural shift.

Going forward, banks will need more targeted deposit strategies, and policymakers must monitor the impact of household savings patterns on the financial system’s stability. RBI may also need to calibrate liquidity support if deposit mobilisation weakens further.

India’s banking sector has managed credit cycles before, but the current funding challenge is deeper and more persistent. Without a stronger deposit base, sustaining the country’s credit momentum will become increasingly difficult.